Where Payment Risk Begins: The Role of Business Structure

Payment risk is often managed at the point where it becomes visible. Teams monitor transactions, review fraud alerts, analyze chargebacks, track approval rates, and respond to partner concerns. This is understandable. Transactions create measurable events, and measurable events are easier to control.

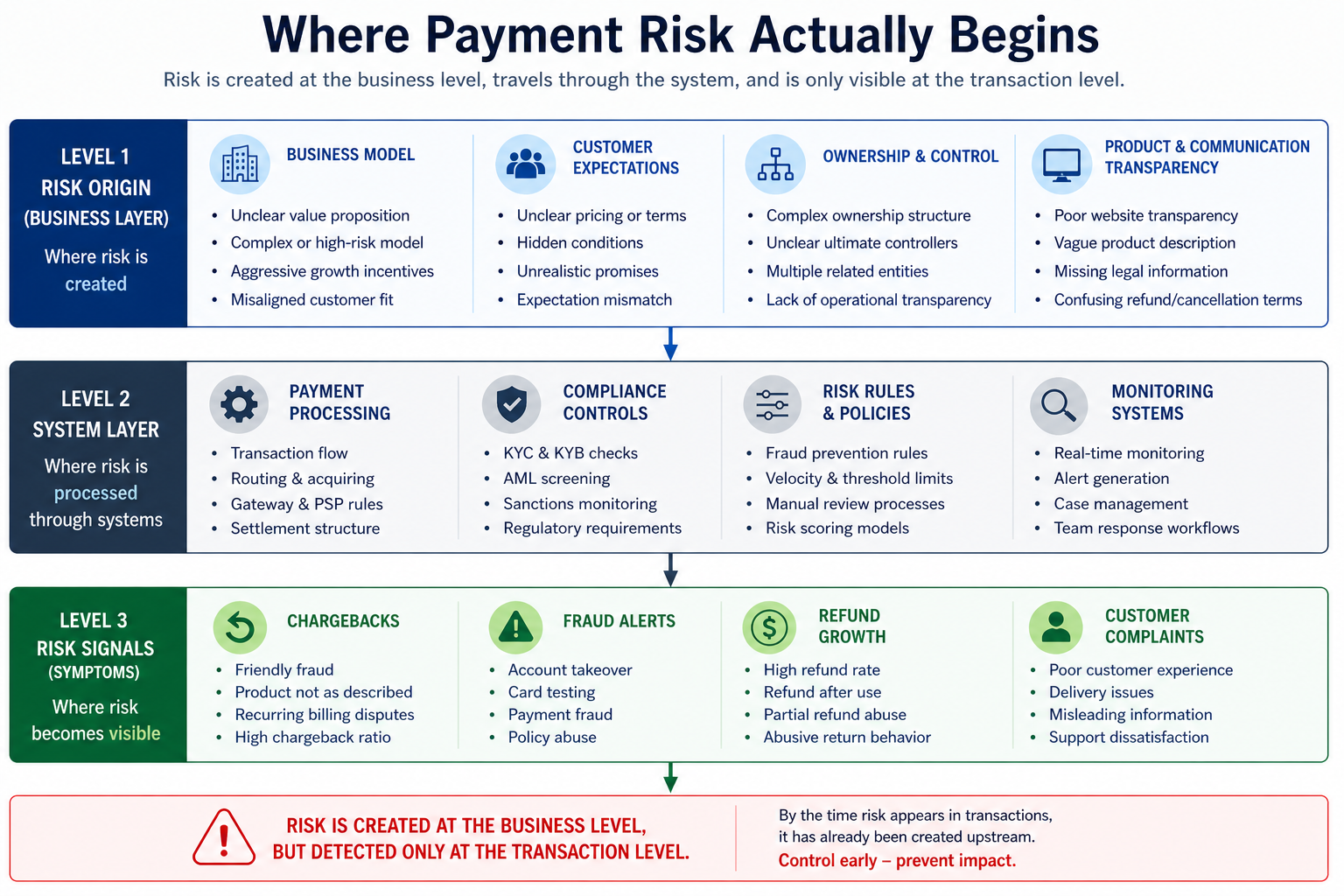

However, this creates a serious limitation. Payment risk is usually detected at the transaction level, but it often begins much earlier. It begins in the structure of the business, the way the offer is presented, the way customers understand the product, the way ownership is organized, and the way operational responsibilities are distributed.

By the time a risk appears in payment data, it may already be the result of decisions made weeks or months earlier. A dispute may look like a customer problem, while the real cause is unclear pricing. A fraud alert may look like a technical issue, while the real weakness is poor merchant screening. A compliance concern may look like a regulatory problem, while the deeper source is an opaque business structure.

This is why strong payment risk management cannot rely only on transaction monitoring. Monitoring is necessary, but it is not enough. Companies need to understand where risk is created before it becomes visible.

This article explains how payment risk originates at the business level, how it travels through systems and controls, and why transaction-level signals often show the final stage of a much longer process.

Risk is usually created before the first transaction

A transaction is not an isolated event. It is the result of a business model, customer journey, product description, pricing logic, onboarding decision, and payment setup. When a customer makes a payment, all of these elements have already shaped the risk profile of that transaction.

For example, a customer may dispute a payment because they do not recognize the merchant descriptor. On the surface, this looks like a chargeback issue. In reality, the problem may have started much earlier, when the merchant failed to explain how the charge would appear on the customer’s bank statement.

Another example is subscription billing. If a customer does not clearly understand renewal terms, the first payment may be approved without any issue. The risk appears later, when the customer sees another charge and files a dispute. The transaction did not create the problem. The unclear customer expectation did.

This distinction matters because different causes require different solutions.

- unclear pricing requires better disclosure

- weak onboarding requires stronger review

- hidden control requires ownership analysis

- customer confusion requires clearer communication

- unstable operations require better processes

If all of these problems are treated only as transaction issues, the company will continue reacting late.

The business layer is where risk is created

The first layer of payment risk is the business itself. This includes the business model, ownership structure, customer expectations, product transparency, pricing, refund terms, and operational logic.

A business can be legally registered, technically integrated, and commercially active while still carrying significant payment risk. The risk may not come from illegal activity. It may come from unclear communication, weak processes, unrealistic customer promises, or a structure that is difficult to understand.

The business layer answers several critical questions:

- what does the customer believe they are buying

- how does the business generate revenue

- who controls the business decisions

- how transparent are the payment terms

- how likely are customers to request refunds

- how stable is the operational model

When these questions are not answered clearly, risk is already present. It may not yet appear in fraud reports or chargeback ratios, but it is embedded in the environment that produces transactions.

This is why business structure should be treated as a risk source, not as background information.

Business model risk is often underestimated

A business model defines how value is created, sold, and monetized. From a payment perspective, it also defines how risk is created.

Some business models are naturally more exposed to disputes, refunds, and customer misunderstanding. This does not mean they are unacceptable. It means they require better controls and clearer expectations.

Examples include:

- subscription services with recurring billing

- digital products with immediate access

- high-ticket services with subjective value

- cross-border offers with mixed customer expectations

- products sold through aggressive advertising

A weak review may classify a merchant by category only. A strong review asks how the model actually works. It looks at the customer journey, billing logic, refund exposure, advertising promises, and expected transaction behavior.

Two merchants may appear similar on paper but create very different payment risk. The difference is usually found in how the business model operates in practice.

Customer expectations are part of risk control

Customer expectations are often treated as a marketing or support issue. In payment risk management, they should be treated as a control issue.

If customers do not understand what they are buying, why they are being charged, how the service works, or what refund rules apply, payment risk increases. This risk may appear later as chargebacks, complaints, refund pressure, or negative feedback.

The transaction itself may look clean. The card is valid, the payment is approved, and no technical fraud signal appears. But if the customer expectation was poorly formed, the risk already exists.

Important expectation-related questions include:

- is the product description clear before payment

- are billing terms visible before checkout

- are recurring payments explained properly

- is the refund policy easy to find

- does the merchant descriptor match customer expectations

- is support available when customers have questions

A company that ignores these questions may later mistake customer confusion for fraud or abuse. That leads to the wrong response. Instead of fixing disclosure, the company may tighten fraud rules. Instead of improving communication, it may increase manual review.

The result is more complexity without solving the root problem.

Ownership and control affect payment behavior

Payment risk is also shaped by who controls the business. Formal ownership is important, but it is not always enough. A company may have declared shareholders while actual decision-making is influenced by other parties, related entities, external operators, or informal controllers.

This matters because control determines behavior. The party that controls traffic, pricing, customer communication, fulfillment, and financial flows has a direct impact on payment risk.

If control is unclear, the payment company may struggle to understand:

- who is responsible for customer issues

- who controls payment flows

- who manages advertising sources

- who decides refund practices

- who benefits from the business activity

When these questions remain open, monitoring becomes less reliable. Transaction data may show what is happening, but not why it is happening.

This is especially important in complex merchant structures, cross-border businesses, and platforms where multiple parties participate in the customer journey.

Hidden structure creates hidden exposure

A business structure may look acceptable on the surface while hiding important risk drivers. Related entities, unclear operational roles, indirect control, and fragmented responsibilities can make risk difficult to interpret.

A detailed discussion of this issue is available in hidden payment risk in business structure, where structural complexity is treated as a direct source of payment exposure.

The key point is simple: if the structure is not understood, the risk is not understood.

A payment company may continue processing transactions while relying on incomplete assumptions about who controls the merchant, how funds move, and why customer behavior looks the way it does.

This does not always create immediate loss. In fact, hidden structural risk may remain quiet for some time. But once volumes grow, complaints increase, or partners ask questions, the lack of understanding becomes expensive.

The system layer processes risk but does not always create it

After risk is created at the business level, it moves into the system layer. This includes payment processing, compliance controls, risk rules, monitoring systems, and operational workflows.

This layer is essential. It decides how transactions are processed, which alerts are generated, how reviews are escalated, and how teams respond to risk.

However, the system layer often processes risk that was created earlier.

For example, compliance controls may detect inconsistencies in merchant data. But the inconsistency may come from a weak onboarding process. Fraud rules may detect unusual transaction patterns. But those patterns may come from a business model that was never fully understood. Monitoring may show rising chargebacks. But the real cause may be poor website transparency.

This means system controls must be connected to upstream analysis. Otherwise, they become reactive.

Compliance can create false confidence

Compliance is a necessary part of payment risk management. Companies must understand regulatory exposure, sanctions risk, AML concerns, documentation quality, and suspicious activity. These controls protect the business and its partners.

But compliance can also create false confidence if it is treated as the complete answer.

A merchant can pass formal compliance checks and still create serious payment risk. Documents may be valid, ownership may be declared, and screening may show no obvious issue. At the same time, the merchant may have unclear billing terms, weak customer support, aggressive traffic sources, or a business model that produces high dispute pressure.

In such cases, the company may feel protected because compliance requirements were met. But the payment risk remains.

This is why compliance should not operate in isolation. It must be connected to operational risk, merchant behavior, customer experience, and transaction outcomes.

The limitations of rigid compliance logic are examined in when compliance starts breaking payment systems, where controls may exist but still fail to address the real source of risk.

Risk rules are only as good as the assumptions behind them

Risk rules are often viewed as objective controls. A rule either triggers or does not trigger. A threshold is either crossed or not crossed. This gives the system a sense of precision.

But rules are built on assumptions.

A rule may assume that certain transaction amounts are suspicious. It may assume that certain geographies are higher risk. It may assume that repeated attempts indicate fraud. These assumptions may be correct in some cases, but wrong in others.

If the business context is missing, rules may misread normal behavior as risky or risky behavior as normal.

This is why rules should not be designed only from historical data. They should be informed by business model analysis, merchant review, customer journey understanding, and operational experience.

Otherwise, risk rules may create friction without improving control.

Monitoring detects signals, not root causes

Monitoring systems are designed to identify changes. They show increases in fraud alerts, refund rates, chargebacks, decline rates, complaints, and other important indicators.

This is valuable. But monitoring does not automatically explain why a signal appears.

A rise in refunds may be caused by abuse, but it may also be caused by unclear product expectations. A decline in approval rates may reflect higher fraud pressure, but it may also result from restrictive rules or poor routing. An increase in complaints may indicate merchant misconduct, but it may also reflect weak support processes.

Monitoring gives visibility. Interpretation requires context.

Without context, companies may respond to signals too narrowly. They may add more controls, increase reviews, or restrict activity without solving the origin of the issue.

The transaction layer shows symptoms

The final layer is where risk becomes visible. This is where the company sees chargebacks, fraud alerts, refund growth, customer complaints, failed payments, and partner concerns.

These signals are important because they show that risk has materialized. But they are often late-stage indicators.

A chargeback does not explain whether the customer was confused, whether the merchant website was unclear, whether the descriptor was misleading, or whether the product failed to meet expectations. A fraud alert does not explain whether the merchant should have been onboarded differently. A compliance escalation does not always explain whether the issue is regulatory, operational, or structural.

The transaction layer is where risk becomes visible, but not necessarily where it becomes understandable.

Why late visibility is expensive

When companies discover risk only at the transaction layer, response becomes more expensive.

At that stage:

- losses may already exist

- customers may already be dissatisfied

- partners may already be concerned

- teams may already be overloaded

- merchant relationships may already be sensitive

The company is no longer making a clean preventive decision. It is trying to reduce damage.

Late action also tends to create internal pressure. Risk teams may recommend restrictions. Commercial teams may resist because the merchant is already active. Operations teams may be handling the consequences. Compliance teams may demand additional documentation.

This creates tension that could often have been reduced by better early understanding.

How companies can move risk control upstream

The strongest payment companies do not wait until risk becomes visible at the transaction level. They move part of the control process upstream.

This does not mean making onboarding unnecessarily slow or blocking every uncertain case. It means asking the right questions early enough.

A more upstream approach includes:

- reviewing the business model before approval

- checking whether customer expectations are clear

- understanding ownership and control

- assessing refund and dispute exposure

- defining expected transaction behavior

- connecting onboarding data with monitoring

This creates a stronger baseline for future decisions. When actual behavior appears, the team can compare it against what was expected.

Without this baseline, every signal is harder to interpret.

Business, compliance, and risk teams need a shared view

One reason payment risk remains fragmented is that different teams often work with different assumptions.

Compliance may focus on documents and screening. Risk may focus on fraud and disputes. Operations may focus on customer cases. Product may focus on conversion. Sales may focus on activation.

Each perspective is valid, but none is complete on its own.

A shared view is needed to understand how business structure affects payment outcomes.

This means teams should connect information such as:

- merchant approval conditions

- customer-facing terms

- ownership and control details

- early transaction behavior

- refund and complaint patterns

- chargeback reasons

When these elements are reviewed together, risk becomes easier to understand and control.

A practical review framework

Companies can use a simple framework to identify where payment risk begins.

Before focusing on transaction signals, the team should ask:

- what business decision created this transaction flow

- what customer expectation was formed before payment

- what ownership or control structure stands behind the merchant

- what operational process affects customer outcomes

- what monitoring signal appeared first

- what late-stage symptom is visible now

This helps separate causes from symptoms.

For example, if chargebacks increase, the team should not immediately assume fraud. It should review the customer journey, refund policy, descriptor clarity, support responsiveness, and merchant onboarding assumptions.

If fraud alerts increase, the team should not only adjust rules. It should ask whether the merchant profile, traffic source, or business model was understood properly.

If compliance concerns increase, the team should not only request more documents. It should ask whether the underlying structure is transparent enough to support safe processing.

What mature payment risk management looks like

Mature payment risk management does not treat risk as a single department’s responsibility. It treats risk as a system.

In such systems, transaction monitoring is connected to onboarding, compliance, merchant review, customer experience, and operational controls.

Mature companies usually follow several principles:

- they identify risk before volume grows

- they define expected behavior before monitoring begins

- they review structure, not only documents

- they connect complaints with customer expectations

- they treat compliance as part of a wider control system

- they revisit assumptions when behavior changes

This approach does not eliminate payment risk. No system can do that. But it helps companies understand risk earlier and respond more accurately.

Conclusion

Payment risk does not usually begin at the transaction level. Transactions reveal risk, but they rarely create it. The real source is often found earlier, in the business model, customer expectations, ownership structure, operational processes, and the way controls are connected.

If a company focuses only on visible transaction signals, it will remain reactive. It may detect fraud, chargebacks, refunds, and complaints, but it will often miss the conditions that created them.

A stronger approach starts upstream. It treats business structure as part of payment risk management. It connects compliance with operations, monitoring with onboarding, and customer outcomes with business decisions.

If your payment environment repeatedly discovers risk only after it appears in transactions, the issue may not be monitoring alone. The weakness may be in the way risk is created, understood, and transferred through the system. A professional audit of payment and risk processes can help identify where business structure, compliance controls, and transaction monitoring are not aligned.