Merchant Verification Layers Before Payment Processing

Merchant verification is often treated as a gateway before payment processing begins. A merchant submits documents, the website is checked, basic ownership information is reviewed, and the business is either approved, rejected, or sent back for clarification. This approach is common, but it is often too narrow.

A proper merchant verification process should do more than confirm that a business exists. It should help a payment company understand what kind of risk is entering the system, how that risk may appear later, and which controls should be applied before the merchant starts processing real transactions.

The difference matters. Many payment problems do not start at the moment of the transaction. They start earlier, when the merchant’s business model is misunderstood, the website is checked too quickly, ownership is accepted without enough analysis, refund terms are unclear, or expected payment behavior is never defined.

Once the merchant is live, these weaknesses become harder to correct. The business has already started processing payments. Customers are already interacting with the product. Banks and payment partners may already be exposed to the risk. At that stage, the company is no longer making a clean approval decision. It is trying to manage consequences.

This is why merchant verification should be understood as a layered process. Each layer answers a different risk question. When all layers are reviewed together, the payment company gets a much clearer view of whether the merchant can be safely accepted, monitored, and scaled.

This article explains the key merchant verification layers before payment processing, why each layer matters, and how weak verification can create long-term payment exposure.

Contents

- Why merchant verification should be layered

- Layer 1: business model verification

- Layer 2: website and customer-facing information

- Layer 3: ownership and control

- Layer 4: product, pricing, and refund logic

- Layer 5: expected payment behavior

- Layer 6: operational readiness

- What happens when verification layers are skipped

- How verification results should affect risk decisions

- How to keep verification useful after approval

- Common mistakes in merchant verification

- A practical merchant verification framework

Why merchant verification should be layered

Merchant verification is sometimes reduced to a checklist. The merchant has a company registration document. The website is online. The declared activity is not obviously prohibited. Ownership information is provided. Contact details exist. On that basis, the merchant may be approved.

These checks are necessary, but they are not sufficient.

A checklist confirms the presence of information. It does not always test whether the information is meaningful, consistent, and useful for risk control. A merchant can provide all required documents and still create serious payment exposure if the business model is unclear, the customer journey is confusing, or the ownership structure does not reflect actual control.

A layered approach works differently. It looks at the merchant from several angles and asks whether the business can be understood in practice.

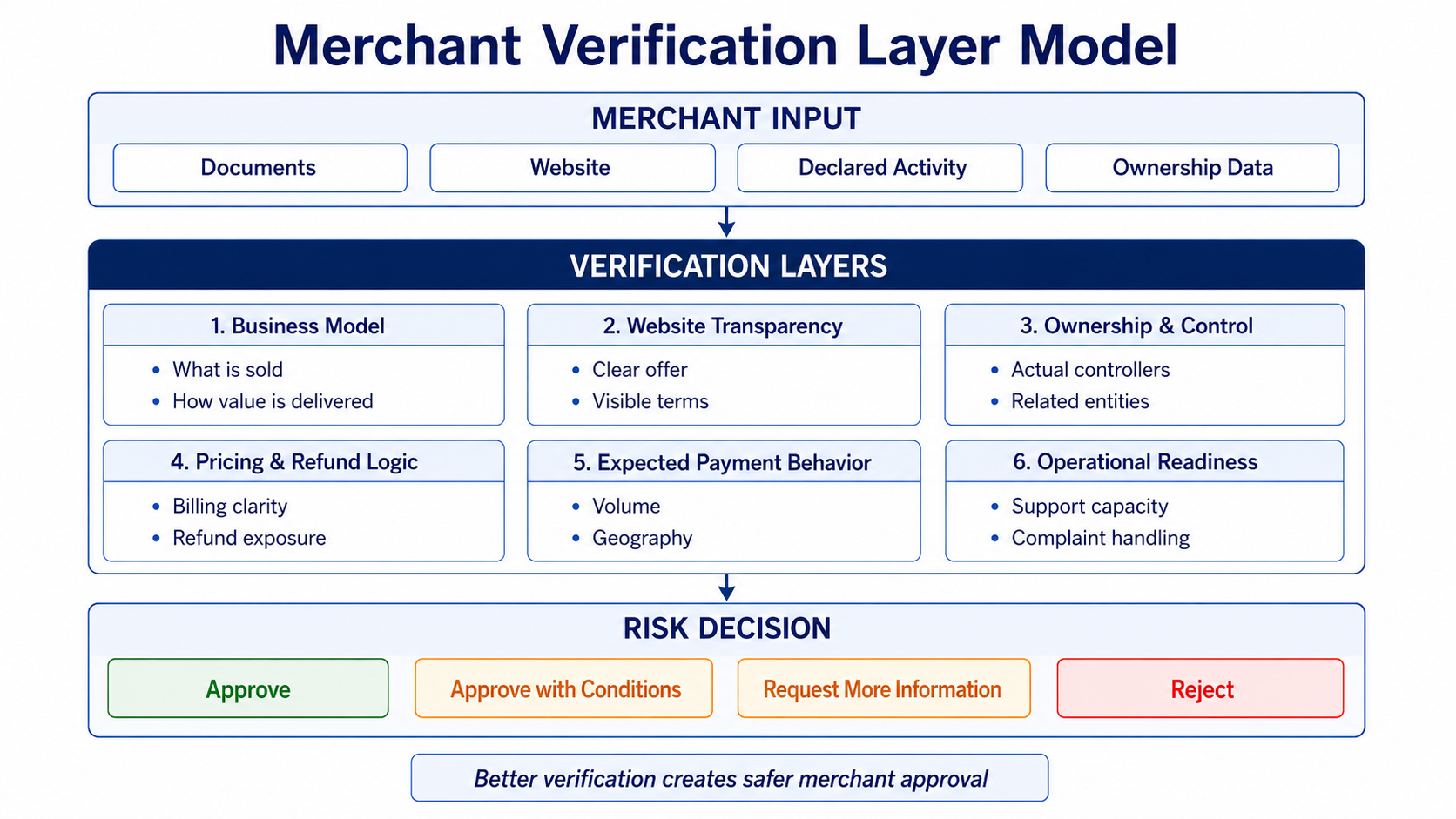

The main layers usually include:

- business model

- website and customer-facing information

- ownership and control

- product, pricing, and refund logic

- expected payment behavior

- operational readiness

Each layer answers a different question. The business model explains what the merchant does. The website shows how the merchant presents the offer to customers. Ownership analysis explains who controls the business. Pricing and refund logic show where disputes may appear. Expected payment behavior creates a baseline for monitoring. Operational readiness shows whether the merchant can handle real customer activity.

When these layers are reviewed separately, important connections can be missed. When they are reviewed together, risk becomes easier to understand.

The layered logic can be visualized as a practical verification model. The merchant first provides input data, then the payment company reviews several risk layers, and only after that makes a risk-based decision about approval, conditions, additional information, or rejection.

Merchant verification should move from basic input data to layered risk review and then to a risk-based decision.

Layer 1: business model verification

The first layer is the business model. Before a payment company approves a merchant, it should understand how the merchant makes money, what is being sold, who the customers are, and why the payment flow exists.

This may sound obvious, but it is one of the most common weaknesses in merchant review. Merchants often describe their activity in broad categories: digital services, online education, consulting, software, marketplace activity, financial services, subscriptions, entertainment, or e-commerce. These categories are useful as a starting point, but they do not define the risk.

The risk is in the details.

A digital service can be transparent and low-risk, or it can be vague, aggressively marketed, difficult to cancel, and likely to generate disputes. A subscription product can be clearly explained, or it can hide renewal terms. A marketplace can have strong seller controls, or it can become a channel for uncontrolled third-party activity.

Business model verification should answer practical questions:

- what exactly does the merchant sell

- why do customers pay for it

- how is the product or service delivered

- how quickly does the customer receive value

- what can create dissatisfaction

- what type of customer behavior should be expected

- does the model create natural refund or dispute pressure

If the payment company cannot explain the business model clearly, it cannot reliably define the merchant’s risk profile.

A strong business model review should also identify whether the merchant’s revenue logic makes sense. If the pricing seems inconsistent with the product, if customer value is difficult to understand, or if the offer depends heavily on aggressive advertising, the merchant may require additional review before processing starts.

Layer 2: website and customer-facing information

The second layer is the website and all customer-facing information. This includes product descriptions, pricing, billing terms, refund policy, cancellation rules, delivery or access conditions, customer support contacts, and any information the customer sees before paying.

A merchant website is not only a marketing asset. It is a risk document.

The website shows what expectations are created before payment. If those expectations are unclear, payment risk increases. A customer who does not understand the product, price, subscription terms, refund conditions, or merchant identity is more likely to complain, request a refund, or file a chargeback later.

Website verification should not stop at checking whether the site exists. A website can be technically functional and still create serious payment exposure.

A proper review should ask:

- is the product or service clearly described

- are prices visible before payment

- are recurring payments explained clearly

- is the refund policy easy to find

- are cancellation conditions realistic

- does the website show reliable contact information

- does the merchant name match what the customer will see after payment

- are delivery or access timelines understandable

The goal is not to judge the design quality of the website. A visually attractive site can still be risky if key information is hidden or vague. The goal is to understand whether a reasonable customer can make an informed payment decision.

This layer is especially important for subscriptions, digital products, online courses, financial services, marketplaces, and businesses where customer expectations are subjective. In these categories, unclear communication can quickly become a payment risk.

Layer 3: ownership and control

The third layer is ownership and control. Payment companies need to know not only which legal entity is applying for processing, but who actually controls the business.

Formal ownership is important, but it does not always explain operational reality. Some merchants operate through related companies, agencies, nominees, traffic partners, external operators, or group structures. In such cases, the party that legally owns the merchant may not be the only party influencing payment behavior.

Ownership and control verification should review:

- declared shareholders

- ultimate beneficial owners

- direct and indirect control

- related entities

- operational partners

- control over traffic sources

- control over pricing and customer communication

- control over settlement and funds flow

This layer matters because control determines future behavior. A merchant’s risk is shaped by the people and entities that make decisions about products, customers, marketing, refunds, and payment flows.

If actual control is unclear, the payment company may struggle later to understand why the merchant behaves in a certain way. Unclear control can also make escalation difficult. When problems appear, the company may not know who is responsible for fixing them.

Complex structures are not automatically suspicious. Many legitimate businesses have several entities or cross-border ownership. The issue is not complexity itself. The issue is unexplained complexity.

If the structure cannot be explained in a practical way, risk remains incomplete.

Layer 4: product, pricing, and refund logic

The fourth layer is the logic of the product, pricing, and refunds. This layer is often underestimated because it appears commercial rather than risk-related. In practice, it directly affects payment outcomes.

A product with unclear value, aggressive pricing, hidden renewal terms, or restrictive refund rules can create future disputes even if the transaction itself is technically clean.

Payment companies should assess:

- whether the product value is objective or subjective

- whether pricing matches customer expectations

- whether free trials or introductory prices are used

- whether recurring billing exists

- whether customers can cancel easily

- whether refund terms are fair and visible

- whether the merchant can process refunds efficiently

This review helps identify where customer dissatisfaction may appear. It also helps the company estimate future dispute exposure.

For example, a high-ticket consulting product may have a different risk profile from a low-cost digital download. A subscription with automatic renewal creates different risk from a one-time purchase. A product with subjective results may create more dissatisfaction than a product with immediate and measurable delivery.

Refund logic is particularly important. If customers cannot understand how to request a refund, or if refunds are slow and difficult, they may go directly to their bank. At that point, the merchant’s weak refund process becomes the payment company’s chargeback problem.

Layer 5: expected payment behavior

The fifth layer is expected payment behavior. Before processing begins, the payment company should define what normal activity should look like for the merchant.

This baseline is essential for monitoring. Without it, unusual behavior is harder to interpret.

Expected behavior may include:

- average transaction amount

- expected monthly volume

- main customer countries

- expected refund level

- expected chargeback exposure

- main payment methods

- expected transaction frequency

- seasonal changes

Different merchants have different normal patterns. A local service provider should not look the same as a global digital platform. A subscription business should not be monitored in the same way as a one-time product seller. A marketplace requires different expectations from a direct merchant.

If expected behavior is not defined, monitoring becomes reactive. The company sees changes but does not know whether they are meaningful.

For example, a sudden increase in international payments may be normal for a merchant launching a global campaign. It may also indicate activity outside the approved business model. Without a baseline, the team may either ignore a real signal or escalate normal behavior unnecessarily.

Defining expected behavior before processing starts helps the company compare what was approved with what actually happens later.

Layer 6: operational readiness

The sixth layer is operational readiness. This layer asks whether the merchant can actually support the payment activity it wants to process.

A merchant can have a legitimate product, clear ownership, and a functional website, but still create payment risk if its operations are weak.

Operational readiness includes:

- customer support capacity

- refund processing capability

- complaint handling

- order fulfillment or service delivery

- internal responsibility for payment issues

- ability to respond to evidence requests

- ability to manage higher volumes

This layer becomes especially important when a merchant expects rapid growth. A business may handle ten customers manually, but fail when it has ten thousand. If support slows down, refunds are delayed, and complaints are not handled, payment risk increases quickly.

Operational weaknesses often become visible only after processing starts. But many of them can be anticipated during verification.

For example, if a merchant has no clear support process, no refund workflow, and no defined responsibility for customer complaints, it is not ready to process significant payment volume safely.

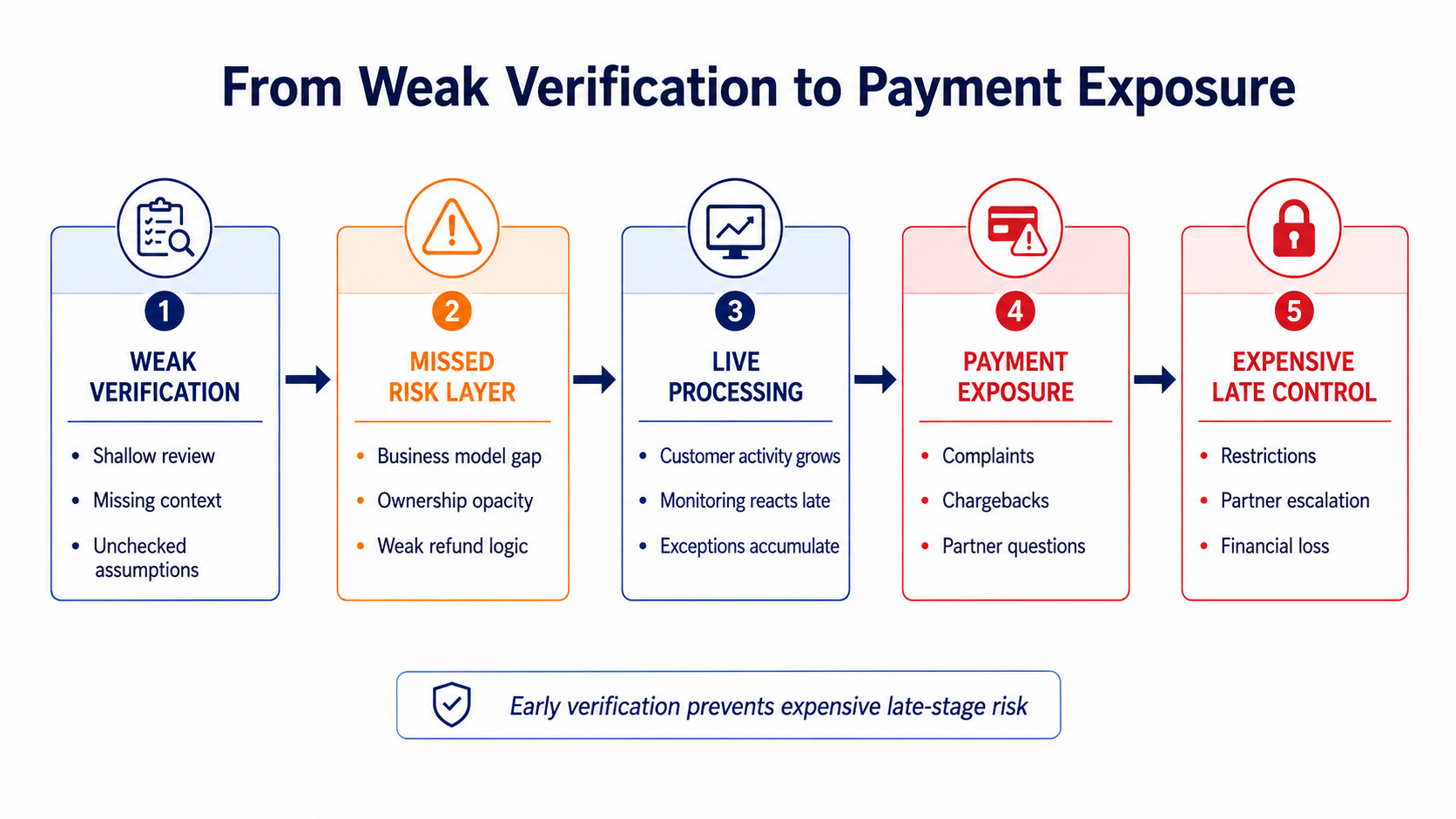

What happens when verification layers are skipped

When verification layers are skipped, payment problems often appear later in forms that look unrelated to onboarding.

A weak business model review may later appear as unusual transaction behavior. A poor website review may appear as customer complaints. Weak ownership analysis may appear as escalation difficulty. Poor refund assessment may appear as chargebacks. Missing expected behavior may appear as monitoring confusion.

This is why weak merchant verification creates long-term exposure. The problem may not appear immediately, but it enters the system at approval.

A detailed explanation of this risk is available in weak merchant checks and long-term payment risk, where shallow review is linked to delayed losses, disputes, and operational pressure.

The most dangerous part is that early activity may look normal. The first transactions may be small. Customers may not complain immediately. Chargebacks may take time to appear. Banks may not ask questions at the start.

This early stability can create false confidence.

By the time problems become visible, the merchant may already have processed volume, developed commercial importance, and created exposure that is harder to reduce.

When verification is shallow, the problem does not always appear immediately. The merchant may start processing normally, but missed risk layers can later turn into customer complaints, chargebacks, partner questions, and expensive late-stage controls.

Weak verification often looks harmless at approval stage, but it can create expensive payment exposure after the merchant goes live.

How verification results should affect risk decisions

Merchant verification should not produce only a simple yes or no decision. A mature process should create a risk-based decision.

Possible outcomes include:

- approval without additional conditions

- approval with lower initial limits

- approval with enhanced monitoring

- request for additional information

- requirement to improve website transparency

- restriction of specific payment methods

- delayed activation until key risks are clarified

- rejection if the risk is unacceptable

This approach is more useful than a binary decision because merchant risk is not always black or white. Some merchants are acceptable with conditions. Some require further explanation. Some can start at low volume but should not scale quickly. Some should be rejected because the risk cannot be understood or controlled.

Verification results should also define monitoring priorities. If the merchant is approved with certain assumptions, those assumptions should be tracked after activation.

For example:

- if refund exposure is a concern, refund behavior should be monitored closely

- if geography is important, actual customer countries should be compared with expectations

- if ownership is complex, control changes should be reviewed

- if the website required changes, those changes should be checked before launch

- if volume is expected to grow, scaling should require reassessment

This is how merchant verification becomes part of an ongoing risk system rather than a one-time approval.

How to keep verification useful after approval

Merchant verification should remain useful after the merchant is approved. The information collected during verification should create a reference point for future monitoring.

The payment company should compare actual behavior with the original assessment.

Important comparisons include:

- declared business model versus actual activity

- expected geography versus real customer locations

- expected volume versus actual processing

- expected refund level versus real refund behavior

- declared website terms versus customer complaints

- declared ownership versus later control changes

This feedback loop helps the company improve future approvals. It also helps identify merchants whose risk profile has changed.

Without this connection, onboarding and monitoring become separate processes. Onboarding approves the merchant, monitoring observes transactions, but nobody compares the two. That gap creates risk.

A stronger system treats merchant verification as the starting point of the relationship. Approval is not the end of review. It is the beginning of controlled observation.

Common mistakes in merchant verification

Several mistakes appear repeatedly in payment environments.

The first mistake is treating documents as proof of low risk. Documents prove existence and may support compliance requirements, but they do not explain how the business behaves.

The second mistake is checking the website only once. Websites change. Pricing pages, product descriptions, subscription terms, and refund policies can all change after approval.

The third mistake is accepting declared ownership without understanding actual control. If another party controls traffic, operations, customer communication, or settlement logic, the formal structure may not tell the full story.

The fourth mistake is failing to define expected payment behavior. Without a baseline, monitoring has no clear reference point.

The fifth mistake is approving exceptions without follow-up. Temporary decisions often become permanent if nobody owns them.

These mistakes are not always dramatic at the beginning. But they weaken the control environment and make future problems harder to understand.

A practical merchant verification framework

A practical framework should be structured, but not unnecessarily heavy. Not every merchant needs the same level of depth. The depth should depend on risk.

A simple model can work as follows.

Low-risk merchants

These merchants may have simple products, clear ownership, transparent websites, predictable geography, and low expected dispute exposure. They can usually go through a lighter review, but the core layers should still be checked.

Medium-risk merchants

These merchants may have subscriptions, cross-border customers, higher transaction values, or more complex refund logic. They require deeper review, especially around website transparency, customer expectations, and monitoring baselines.

Higher-risk merchants

These merchants may have complex ownership, unclear products, aggressive marketing, unusual payment flows, sensitive categories, or rapid expected growth. They require enhanced verification, stricter conditions, and ongoing monitoring.

The purpose is not to slow every merchant. The purpose is to match verification depth with actual exposure.

Conclusion

Merchant verification before payment processing should not be a simple checklist. It should be a layered process that helps the payment company understand the business before exposure begins.

The key layers include the business model, website transparency, ownership and control, product and refund logic, expected payment behavior, and operational readiness. When these layers are reviewed together, the company can make better decisions about approval, limits, monitoring, and scaling.

Weak verification does not always create immediate loss. It often creates delayed risk. The merchant may look normal at the beginning, but hidden weaknesses can later appear as disputes, refunds, complaints, chargebacks, or partner pressure.

A stronger verification process helps prevent this. It gives the company a clearer understanding of what kind of merchant is entering the system and what needs to be monitored after approval.

If your payment business needs to review merchants more effectively, identify hidden risks before activation, or strengthen merchant onboarding and verification controls, learn more about professional Merchant Risk Assessment and Compliance Verification.